Introduction: Why So Many People Are Living Paycheck to Paycheck in 2026

Living paycheck to paycheck means that nearly every dollar you earn is already spoken for before it even reaches your bank account. Rent, groceries, utilities, insurance, transportation — the money disappears fast. One unexpected expense can be enough to derail the entire month.

If that sounds familiar, you’re not alone.

In 2025, millions of people in the U.S. are stuck in this cycle. Rising housing costs, inflation, student loans, medical expenses, and credit card debt have made financial stability feel out of reach — especially for young adults and working families.

But here’s the truth most people don’t hear enough:

Living paycheck to paycheck is not a personal failure. It’s a systems problem — and systems can be changed.

This guide will show you exactly how to break the paycheck-to-paycheck cycle step by step, even if your income feels low right now. No fluff. No unrealistic “just earn more” advice. Just practical moves that work in real life.

Quick note before we start: If you’re here because your budget never seems to “stick,” you’re probably dealing with a cash flow problem (timing + fixed bills), not a willpower problem. We’ll fix that too.

What Does Living Paycheck to Paycheck Really Mean?

Living paycheck to paycheck means you depend on your next paycheck to cover basic expenses. There’s little or no margin for error.

Common signs include:

- No emergency savings (or it gets wiped out constantly)

- Using credit cards to pay for essentials

- Stress spikes before payday

- Avoiding checking your bank balance

- Feeling stuck despite working hard

- Paying bills late because the paycheck timing doesn’t match due dates

This is not just a budgeting issue. It’s a stability issue — often a combination of cash flow, debt, irregular expenses, and (very often) unpredictable income.

How Many Americans Are Living Paycheck to Paycheck in 2026?

While exact numbers vary depending on how “paycheck to paycheck” is defined, the underlying picture is consistent: a large portion of U.S. households struggle to save regularly and rely on their next paycheck to cover necessities.

This is especially common among:

- Renters in high-cost metro areas

- Young adults early in their careers

- Hourly workers with variable schedules

- Gig workers and freelancers

- Families with childcare costs

- People carrying high-interest debt (especially credit cards)

And here’s the important part: you can be “doing everything right” and still feel stuck because modern expenses are front-loaded and inflexible (rent, insurance, healthcare), while wages are often slow to catch up.

So if you feel ashamed, drop that. Shame doesn’t build savings. Systems do.

According to recent data on household financial stress in the U.S., many Americans struggle to save consistently.

Budgeting vs Cash Flow: Why Budgeting Alone Is Not Enough

Most advice tells you to “make a budget.” That’s not bad advice — it’s incomplete.

Budgeting answers:

“Where should my money go?”

Cash flow answers:

“Do I have enough money at the right time to pay bills without panic?”

If your rent is due on the 1st but you get paid on the 5th, a perfect budget can still fail. If your pay varies each week, “monthly budgeting” can feel like guessing.

When people say:

- “I keep breaking my budget”

- “Budgeting doesn’t work for me”

- “I’m disciplined but still broke”

…they’re usually dealing with cash flow mismatches, fixed expenses that are too high, or debt payments that eat the margin.

This guide fixes the system, not just the spreadsheet.

Why Breaking the Paycheck-to-Paycheck Cycle Is So Hard

1) Fixed Expenses Dominate Income

Housing, utilities, insurance, and minimum debt payments often consume most of your paycheck immediately.

2) Inflation and Cost of Living Pressure

Even small increases (groceries, gas, subscriptions) quietly erode any margin you build.

3) Irregular Expenses Are “Silent Killers”

Car repairs, medical co-pays, gifts, travel, annual fees — these don’t happen monthly, but they happen.

4) Psychological Stress and Decision Fatigue

Constant money stress creates a loop:

- stress → avoidance → late fees → more stress

or - stress → impulsive spending → regret → more stress

5) No Buffer Turns Every Surprise Into Debt

Without savings, every unexpected bill becomes credit card debt — and high interest keeps you trapped.

The way out is boring, structured, and extremely effective: stabilize first, then optimize.

Step 1: Build a Survival Budget (Not a Perfect One)

If you’re living paycheck to paycheck, your goal is not “the ideal budget.” Your goal is not falling behind.

A survival budget focuses on:

- covering essentials

- stopping new debt

- creating breathing room

- making the month predictable

Essentials (Needs)

- Housing (rent/mortgage)

- Groceries (basic, not luxury)

- Utilities (electric, water, internet)

- Transportation (gas/public transit)

- Minimum debt payments

- Healthcare basics

Non-Essentials (Wants)

- Dining out

- Entertainment

- Shopping

- Subscriptions

Financial Basics

- Emergency savings (small at first)

- Extra debt payments (later)

Pro tip: If you feel overwhelmed, don’t start by tracking everything. Start by listing your top 8–12 recurring bills and their due dates. Survival budgeting is more about priority order than perfection.

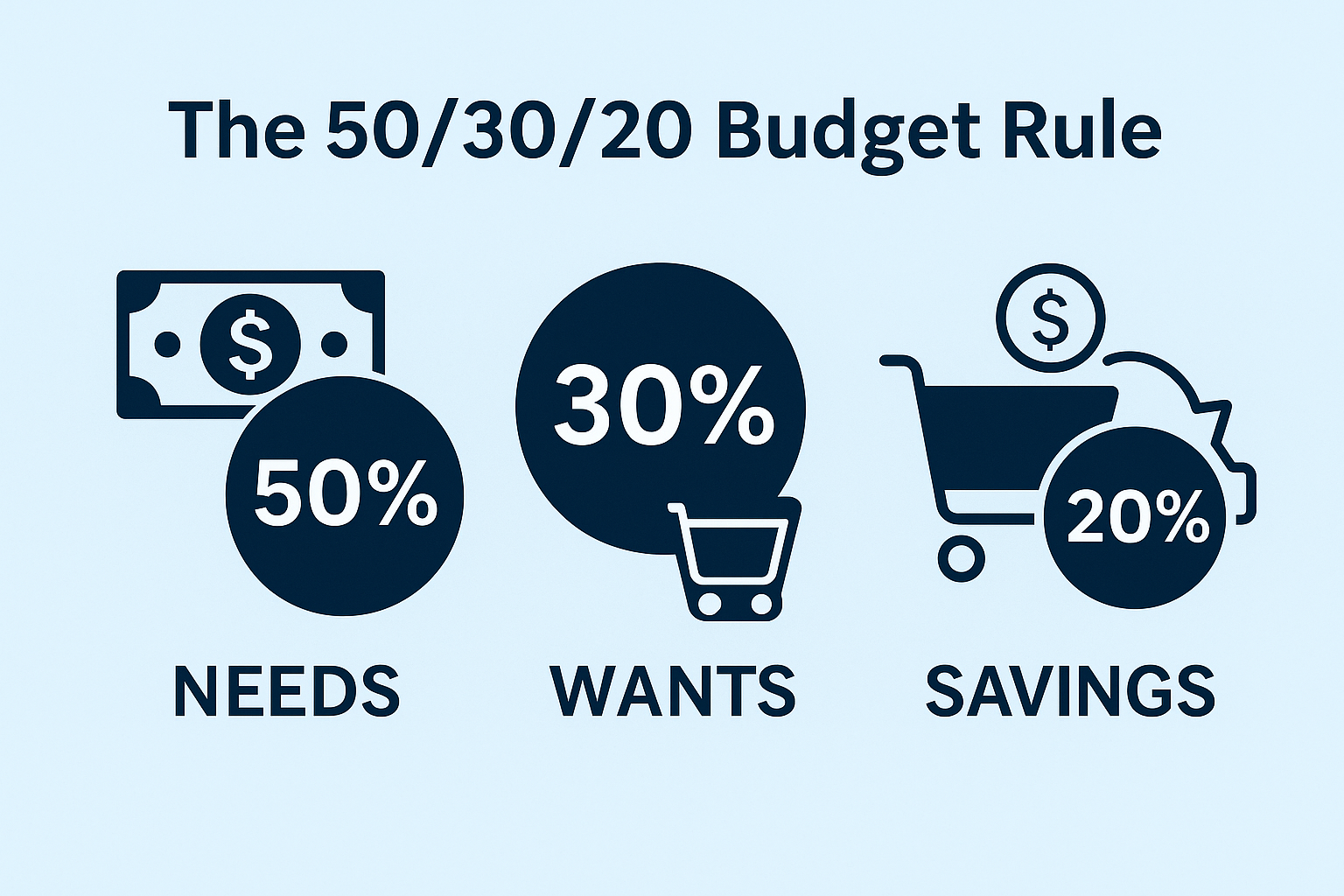

👉 For a beginner-friendly structure, link this inside your article:

The 50/30/20 Budget Rule Explained for Beginners

Mini action (15 minutes):

Write down:

- Your monthly income after taxes (or your average)

- Your “must-pay” bills

- The gap (if any)

If there’s no gap, don’t panic — it means you need Step 3 and Step 8 sooner.

Step 2: Fix Paycheck Timing (The Hidden Breakthrough)

This step is underrated: many people stay trapped because of bill timing.

Try these fixes:

- Call lenders and utilities to adjust due dates closer to payday

- Split rent payments (some landlords allow half on the 1st, half mid-month)

- Move subscriptions and smaller bills to the week after payday

- Use one “Bills” account and pay everything from it

Even shifting 2–3 due dates can reduce late fees, overdrafts, and stress.

If you’ve never tried it, you’ll be surprised how often companies will work with you.

Step 3: Automate Small Savings to Build Momentum (Even $10)

Saving feels impossible when money is tight. But the habit is what breaks the cycle.

Start with:

- $10–$20 per week

- automated transfer on payday

- separate savings account (not your main checking)

This creates:

- a mini buffer against surprises

- reduced anxiety

- proof you’re moving forward

If you can’t save weekly, save per paycheck:

- $5 per paycheck is still a win

👉 Add this internal link naturally:

Emergency Fund 101: How Much Do You Really Need?

Step 4: Cut Only High-Impact Expenses (Ignore the Small Stuff)

If you try to cut everything, you’ll burn out. Most people do.

Instead, target the big 3:

- Housing

- Transportation

- Food

Housing (biggest lever)

Options (choose one realistic):

- roommate for 6–12 months

- negotiate renewal terms early

- downsize if your rent is crushing your budget

- consider moving slightly outside expensive areas

Even a $150–$300 reduction is life-changing long-term.

Transportation

- public transit (if possible)

- carpool

- consolidate errands (reduce gas)

- avoid “new car payment traps” if your budget is tight

Food

Meal prep isn’t glamorous — it’s powerful.

- plan 2–3 cheap meals

- repeat them weekly

- use store brands

- reduce takeout “because tired” spending

👉 You already have the perfect satélite for this step:

Low-Income Budget Hacks That Actually Work (2025 Guide)

Step 5: Use a Simple Spending System (So You Don’t Need Willpower)

You don’t need discipline. You need friction.

Option A: The “Cash Cap” System

After bills + groceries:

- withdraw a fixed amount in cash ($60–$150 depending on your situation)

- that’s your flexible spending

- when it’s gone, spending stops

This reduces impulse spending because the money is visible.

Option B: Envelope Batching (3 Categories Only)

Create only:

- Food

- Transportation

- Everything Else

Fund weekly, not monthly. Weekly planning works better for paycheck-to-paycheck life.

Option C: “One Card Only” Rule

If credit cards trigger overspending:

- keep one card for autopay bills only

- keep daily spending on debit/cash

- remove saved cards from online shopping

These systems reduce mistakes without requiring perfection.

Step 6: Stop the Debt Spiral (Without Feeling Hopeless)

Debt keeps people living paycheck to paycheck because it steals future income.

Start simple:

- pay minimums on everything

- attack one debt with any extra money

The “Tiny Wins” Method

- Choose the smallest balance

- Pay $10–$30 extra each month

- Track the progress visibly

- When it’s cleared, roll that payment into the next debt

It’s not mathematically perfect — it’s psychologically effective, which matters when you’re stressed.

👉 Add your internal link here:

How to Pay Off Credit Card Debt Fast in 2025

Avoid this mistake:

Don’t use a 0% balance transfer if you’re still overspending — you’ll just rebuild the debt.

Step 7: Build Credit While Living Paycheck to Paycheck (Cheap + Simple)

Good credit is a wealth tool. Bad credit is a wealth drain.

The simplest strategy:

- one small purchase per month (gas, phone bill, etc.)

- pay in full every month

- keep utilization under 10–30%

- never miss a payment

This builds credit without paying interest.

👉 Add this internal link:

How to Build Good Credit from Scratch

Why it matters: Better credit = lower interest rates = cheaper car insurance and loans = more margin.

Step 8: Plan for Irregular and Annual Expenses (The Quiet Budget Killers)

Most budgets collapse because people ignore non-monthly costs:

- car maintenance

- medical visits

- annual subscriptions

- gifts

- travel

- insurance renewals

Fix:

- List your irregular expenses

- Estimate the yearly total

- Divide by 12

- Auto-save monthly into a “Future Bills” account

Example:

- $600 car insurance annually → $50/month

- $120 Prime annually → $10/month

This turns chaos into a predictable system.

Step 9: Increase Income in Small, Realistic Steps (The Fastest Escape)

Expense cuts have a ceiling. Income increases don’t.

Your goal isn’t “get rich.” Your goal is:

create an extra $200–$500/month margin

That margin becomes:

- savings

- debt payoff

- stability

Low-barrier ways to increase income:

- AI-assisted freelancing (writing, design, simple admin tasks)

- microtasks

- online reselling (Facebook Marketplace, eBay)

- selling templates (Notion, resumes, spreadsheets)

- gig apps (if the math works in your area)

Rule: only do side hustles that don’t require upfront money you don’t have.

👉 Add your internal link:

How to Start a Profitable Side Hustle in 2025

Step 10: Build a Starter Emergency Fund ($300–$500)

You don’t need a full emergency fund right away. You need protection.

A $300–$500 starter buffer prevents:

- a $200 car repair becoming a $1,200 credit card problem

- medical co-pays triggering debt

- overdrafts and late fees

Once your starter fund is built, you can expand to 1 month of expenses, then 3 months over time.

👉 Internal link again (good to repeat once in a long pillar):

Emergency Fund 101: How Much Do You Really Need?

Step 11: Upgrade Your Money Habits (So It Sticks)

Breaking the cycle isn’t only math. It’s behavior + environment.

Useful habits:

- check your balance once daily (2 minutes)

- weekly “money reset” every Sunday (10 minutes)

- one “no-spend day” per week

- unsubscribe from marketing emails and remove saved cards

- keep goals visible (debt payoff tracker, savings tracker)

👉 You can link here:

7 Financial Habits That Will Make You Rich Over Time

Habits are the glue. Without them, progress resets.

Common Mistakes That Keep People Living Paycheck to Paycheck

1) Trying to Budget Perfectly

Perfection kills consistency. Survival budgeting wins.

2) Ignoring Irregular Expenses

If you don’t plan for them, they become debt.

3) Using Credit Cards as Income

Credit cards are not income. They’re delayed pain.

4) Cutting Everything Instead of the Big Levers

Don’t torture yourself over small purchases while rent destroys your budget.

5) Depending on Motivation

Motivation fades. Systems survive.

6) Upgrading Lifestyle Too Soon

If you get a raise and upgrade expenses instantly, you stay trapped.

How Long Does It Take to Stop Living Paycheck to Paycheck?

This depends on your starting point, but here’s a realistic timeline:

First 30 Days

- survival budget in place

- fewer “surprise” overdrafts

- spending becomes more visible

- small savings habit starts

By 90 Days

- starter emergency buffer built (or close)

- fewer panic moments

- one debt balance starts shrinking

- spending control systems feel normal

6–12 Months

- real stability for many people

- better credit

- more consistent savings

- less financial stress overall

Progress is not linear. But consistency compounds.

FAQ

Can you stop living paycheck to paycheck on a low income?

Yes. Income matters, but better systems (cash flow, spending control, small savings, and debt management) can dramatically improve stability even before a big raise.

Should I save or pay debt first?

Build a small starter emergency fund first ($300–$500), then focus on high-interest debt. Without a buffer, you’ll keep falling back into debt.

What is the best budgeting method if my income changes weekly?

Use a weekly budget based on your lowest expected income. Separate essentials from flexible spending and fund categories weekly.

Is living paycheck to paycheck normal in the U.S.?

It’s common — but “common” doesn’t mean “permanent.” A systems approach can break the cycle.

Do budgeting apps really help?

They help with awareness, but tools don’t fix behavior by themselves. Pair apps with a simple spending system (cash cap or envelope batching).

How much should I save if I truly can’t afford it?

Start extremely small: $5 per paycheck. The habit is the goal at first, not the amount.

How can I reduce stress while fixing my finances?

Focus on the next step only: build a survival budget, then a small buffer. Stability reduces stress faster than complicated plans.

Conclusion: You Can Break the Cycle — Step by Step

Living paycheck to paycheck is exhausting. It drains your energy, your confidence, and your ability to plan.

But it’s not permanent.

If you build a survival budget, control the biggest expenses, stop the debt spiral, and create even a small financial buffer, you will start to feel the difference — often within weeks.

You don’t need perfection.

You don’t need a massive raise tomorrow.

You need the right system — and the patience to run it consistently.

And now you have it.

Pingback: How to create a monthly budget that works in 2025

Pingback: Emergency Fund 101: How Much Do You Really Need? - Prime Finance Insights